What is a Business Continuity Plan & Why is it Important for your Business?

What is a Business Continuity Plan & Why is it Important for your Business?

As a business owner, there are many factors to consider when keeping your operations running smoothly. That said, the past year has been unlike any other, we as a society, have experienced in recent times.Part of ensuring that your business continues to operate during times of upheaval, such as other types of sudden events like natural disasters, ice storms, fires, and floods, etc. - it is critical to have what is known as a Business Continuity Plan.

Business Continuity Plans are crucial to a company’s ability to survive and be sustainable during times of crisis that would otherwise significantly interrupt and impede their day-to-day operations. On the other hand, companies who have the foresight to put key plans in place, in order to offset the devastating consequences that these types of occurrences, can go on to operate another day.

Fortunately, as a business owner in Canada, you are not alone in making these vital and strategic decisions. Public Safety Canada, through the Government of Canada has helped by outlining some key aspects of this process.

First of all, it is suggested that you start by identifying the severity of these types of potential threats to your business. Next you can look at narrowing down which specific ones will require that you implement a proactive plan. It is also important to determine which of these aspects will require documented follow-up tasks, and what steps will need to be taken as a result.

Here are some valuable considerations you can ask yourself as you begin to develop your own business continuity plan model.

Do you have enough Insurance?

Another fundamental part of this plan is to ensure you have the right insurance coverage for your business needs. In your business continuity plan, you will want to examine your current insurance coverage and make sure that it will include these types of events and will adequately cover the cost of any major potential losses you could encounter.

It can also be equally important to look at whether you are overinsured in any areas that perhaps will not pertain to your business. Ultimately, at this stage as well as on a regular basis, it is important to reevaluate your business insurance coverage in order to ensure your continuity plan is highly reflective of your business operations, not to mention a proactive plan for future sustainability.

In the event of a disaster and when the continuity plan needs to be implemented, it is necessary to set up a method for informing your business associates, staff, suppliers, and clients. Safety procedures are also a part of these plans, so that the well-being of staff and clients are maintained, and business operations and connections are preserved as much as possible when and if, the time comes that the continuity plan must be activated.

As you act to either develop or re-visit your Business Continuity Plan, it is important to understand that having the right insurance can also play a large role in the success of this plan.

One step you can take right now is to reach out to your insurance broker to discuss your current insurance coverage. Contact Leaders Insurance to find out more about how we can contribute to the successful future of your business.

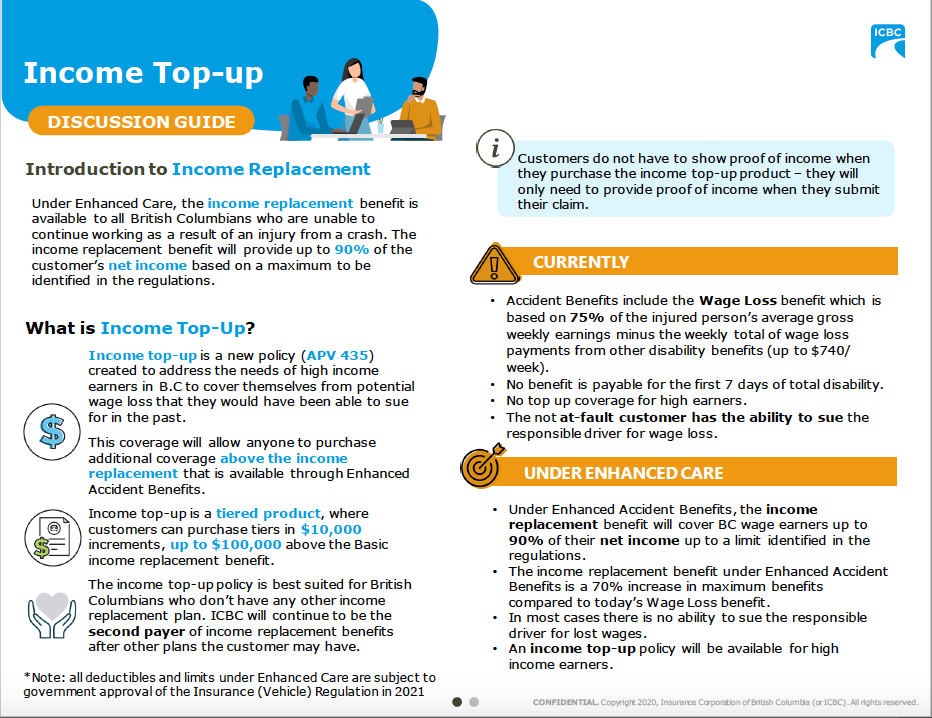

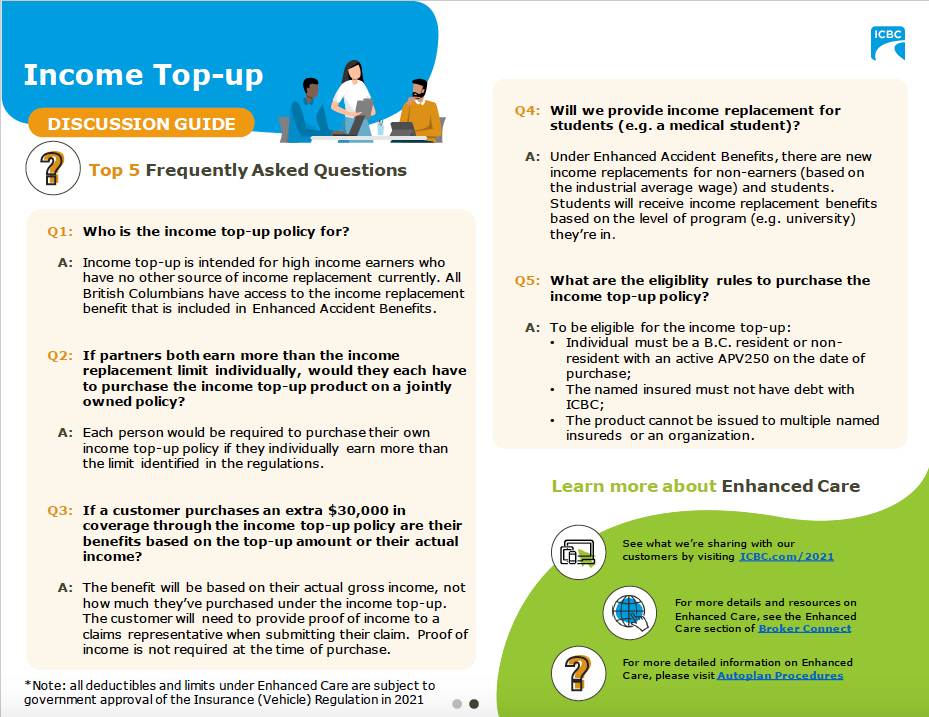

NEW Enhanced Care Coverage Offered by ICBC - starting May 2021

Starting May 2021, ICBC will be offering Enhanced Care Coverage which is a Income Top-Up program for individuals involved in an accident where they will have loss of work. To find out more, please contact us at 604-469-1799 or read the information sheets below -

For more information on Enhanced Care, click here.

How to Insure a Vacation Home in 2021

How to Insure a Vacation Home in 2021

Do you own a vacation home? If so, then 2021 as well as its predecessor, may have posed some additional challenges for you with regards to either operating it as a rental or being able to spend some time there, yourself. Hopefully this will improve as we move further in 2021, however, one factor still remains the same, you will need to continue to have this property adequately insured.Here are a variety of scenarios that may relate to you and your vacation home and the steps you can take to ensure you have the proper home insurance policy to meet your ongoing needs.

For starters, to help determine the type of insurance you need, one key consideration is how often you will be living there. For example, if this is your secondary residence, then it is important to know that it is likely that you will be paying a bit more for insurance costs. In some cases however, you may be able to include your vacation home insurance in the same policy with your primary residence coverage.

To better identify how best to insure your vacation home, you can review the following vacation home occupancy scenarios and see which one(s) best reflect your insurance needs.

Insuring a Home You Are Not Renting Out

If you own a vacation home that you are not going to be renting out, then your primary home insurance coverage may not include this type of coverage. This is because primary residence insurance policies typically only relates to homes that are being regularly occupied.

For example, if this home will be unoccupied for more that 30-90 days at a time, you are likely to need to take on some additional coverage to include in your home insurance package. Speaking to your insurance broker is the best course of action, so that you make sure you have enough secondary coverage.

Insuring a Home You Will Occasionally Rent Out

This second scenario includes the times when you plan to rent out your secondary residence on an occasional basis. Perhaps you will rent out your vacation home as an occasional Airbnb, or to friends and family a couple of times a year.

If this is the case, then your original and standard home insurance policy might cover this type of arrangement as well. With that said, again you will want to discuss this with your home insurance broker to ensure you have the right coverage for your needs.

Insuring a Home You Will Regularly Rent Out

This last rental arrangement, as the heading states, is for secondary vacation homes that will be rented out on a regular basis. Unlike the other two scenarios, if this is your plan, it is highly likely that you will need to add some additional coverage onto your original policy.

Here are some of the types of supplemental coverage you may need, depending on your circumstances.

Short-Term Rental Insurance Coverage:

Otherwise known as home-share coverage, this vacation home insurance policy option is typically a type of insurance for those who are renting out their homes as an Airbnb or for shorter periods of time. In this type of arrangement, adding coverage to your original policy is the likely to be necessary. It is advisable that you check with your broker make sure you have enough insurance for the correct length of time for these shorter rental periods.

Long-Term Rental (Landlord Insurance) Coverage:

This type of coverage is used more in the cases of longer-term rentals, however sometimes can also apply to short-term tenants as well. If there is the potential that you will be renting out your vacation home for longer stretches of time, then choosing this comprehensive insurance package might be the more affordable option. This insurance policy reflects a separate insurance package on its own to ensure that as a homeowner you are adequately covered for these types of rental agreements.

In the end, the best way to protect your vacation home is to first, identify how you plan to rent out your vacation home in the future. Additionally, since these types of insurance policies can vary across different insurance companies, you will want to examine these policies closely with the help of your insurance broker.

At Leaders Insurance we want to ensure that our clients have the most up-to-date information regarding their insurance policies. If you are looking to insure your vacation home this year, contact us so that we can align your home insurance coverage with your specific needs.

What is a Communicable Disease Exclusion on your Home Insurance?

What is a Communicable Disease Exclusion on your Home Insurance?

If you are a homeowner, it is likely that you have already given a lot of thought to the type of insurance you need. With that being said, these days, we have had to expand our scope more than ever to also factor in issues related to COVID-19 and pandemic home insurance claims.There is a component of home insurance that covers Communicable Disease Exclusion, and while in the past, this has been rarer, during these unprecedented times, some insurance companies have opted to include this in their home insurance policies moving forward.

Currently this type of insurance feature has been closely related to the COVID-19 claims that insurance companies are more likely to encounter. For example, in the event a person files a claim that they have been infected with COVID-19 or another communicable disease in the home of another individual, they could feel they have grounds to sue the individual whom feel is responsible, particularly if they have become severely ill as a result.

While in many parts of Canada, there have been strict rules in place for limiting gatherings, particularly within homes. This type of cross-household contact has been identified as one of the common methods of COVID-19 transmission.

On the other hand, many Canadians have taken the necessary precautions and done everything possible to avoid the spread of COVID-19. With that said, individuals could still have gone on to contract the virus and in some cases, they may look at tracing it back to a certain social gathering or interaction they had within a particular household.

While it can be a challenge to prove these types of cases, the bottom line is, that this could be an expensive outcome for homeowners. Therefore, turning to this type of home insurance coverage may definitely be worth examining further.

Ultimately, with this Communicable Disease Exclusion in place, your home insurance policy can cover these types legal expenses. It is recommended that you do reach out to your broker to find out if this is already included in your policy, and if not, perhaps adding this your home insurance package could be of great benefit to you.

In the end, what this really comes down to is the importance of having a full understanding of your home insurance policy. By having a better grasp of all of the features and specific types of coverage, as a homeowner, you can have the added peace of mind you need to effectively navigate the responsibilities of homeownership, especially during these extremely challenging times.

At Leaders Insurance, we are committed to making sure our clients are informed and fully satisfied with their insurance coverage. Contact us today to learn more about the Communicable Disease Exclusion for homeowners, and let us help to ensure you are set up with the best home insurance policy that covers all of your needs now and into the future.

BC Strata Insurance Market 2021

BC Strata Insurance Market 2021

While strata housing can range from various dwellings, that include condos, duplexes, and single detached family homes, this type of housing has its own set of unique features. In BC, there are over 1.5 million individuals living in this type of living arrangement, which involves both homeowners and property space, that offers various shared amenities in the community setting.

With that being said, along with these shared amenities, which can in certain cases include, pools, recreation and fitness centres, and shared green spaces, there are of course fees that go along with these types of offerings, including ion course insurance premiums.

While, having the proper insurance is always the best course of action to ensure we are protected when in comes to various financial and personal aspects of our lives, the BC Strata Insurance market has seen an incredible surge in the cost of these fees over the past year. In fact, these figures have reached double and tripled digit percentage margins in only a short period of time.

With strata corporations across BC looking to obtain affordable coverage for their properties, this has proven no easy task as the demand and the costs continue to be high. Some direct causes have been identified by the BC Financial Services Authority (BCFSA), which points out that a recent 10 year stretch of a softer housing market, which then turned quickly into what is know as a hard market. With this now being the reality, many insurers have had to look for ways to meet their profitability margins.

In turn, with less insurers in the game, and more properties to insure, more risk has been taken on, and this has ultimately driven up these prices. Claim costs have also risen and this has led to more insurance fees throughout the Strata Market.

With current premium and deductible insurance fees somewhat levelling out, this still does reflect higher levels than ever before. Now with only a little over a month into 2021, there is no sign that these fees will be decreasing any time soon.

Fortunately however, some necessary steps have been outlined as a way of improving these conditions. The BC Government has outlined some key areas that need to be taken into account when looking to regulate the procedures used to guide strata corporations. With the current high costs that strata members are facing when paying for insurance, this key issue is also at the heart of these new regulations.

While best price quotes are one of these necessary changes that should be addressed to bring down these premiums, it is still the costs associated with home-related insurance claims that have been identified as the bigger culprit. By bringing these down, it is suggest by the BC Financial Services Authority (BCFSA), the Strata Insurance market should thankfully experience some more affordable prices in the future.