2021 Condo insurance Update

2021 Condo insurance Update

Here is an update on the status of the Condo Insurance and BC Strata Market for 2021.

New information on the progress being made in this area has recently been released. This information is sure to have many BC condo owners asking the fundamentally important question of whether these premiums will continue to increase – or if BC will finally see a welcomed decrease in these rates anytime soon!

At first glance, the situation appears to remain much the same as insurance prices continue to be high in the province. As previously reported, the BC government’s Financial Services Authority (BCFSA) has been preparing to enact new strata corporation rules that are designed to lower these rates. On that note, it appears the exact timeframe for these additional regulations is still unclear.

With household claims being said to remain a huge factor in these increases, especially as many of the complexes continue to age, it is even the units where claims have not been made, that are also negatively impacted by these continually high rates.

To put the nature of these sharp increases into perspective, in areas such as Surrey, one townhouse complex reportedly saw premium increases of 180 percent in 2020. Moreover, it has been estimated that at the same location, rates are set to rise again this year by a total of 70 percent. While on one hand, the increase this year appears to be less, it is still an increase none-the-less that has many BC home owners extremely concerned.

Experts report that even if rates start to come down slightly, there are millions of BC residents who live in strata complexes, who need to see a sharp downwards turn in this market for them to experience some significant financial relief.

Ultimately, this remains a multi-faceted issue, with the BC government continuing to work to implement more changes. That said, it has been revealed that more regulations are coming in the future to help stabilize this market.

The group at the head of this change policy, the BCFSA believes that this market can be tamed, however it has become clear that this system will likely take time to correct.

The competitiveness of home insurance availability also points to driving up these fees. With limited insurance options at this point in time for condo corporations, some experts are stating that a return to private insurance companies may be the best course of action as another counteractive solution to the climbing rates in BC.

As BC residents await these previously announced regulations, it is clear that there remains an overall consensus that in order to ensure that a return to a healthier condo insurance market can occur as soon as possible, these government changes cannot come soon enough.

While navigating the current housing market, turning to an insurance agent remains an effective method of ensuring you have access to the best insurance options. Contact Leaders Insurance for more information on how we can provide you with the home insurance you need.

The Role Insurance Agents Play for your Car Insurance

The Role Insurance Agents Play for Your Car Insurance

If you have car insurance on your mind, it is also likely that there are many questions running through your head. That said, one very important part of this process is to seek out the help of a quality vehicle insurance agent.Here are some key pieces of information about how to identify the role an insurance agent can play in making this a successful experience for you, as well as what to look for when choosing the most suitable broker for your car insurance needs.

The Benefits of Working with an Insurance Agent Helping to Understand Your Insurance Policy

Turning to an insurance agent is a great place to start as they are the experts in their field. The reality is that it can be a bit overwhelming to make decisions that directly affect you financially, especially since insurance typically covers a lot of different facets. However, with the support of insurance agents, you can be more well-informed about your insurance options, and ultimately, more confident in your financial decisions.

Identifying the Proper Coverage

Insurance agents can also help direct you to the most suitable insurance packages for your needs. Depending on your vehicle, your safety, and your financial parameters, an agent can help to ensure you have the proper coverage. As a result, this can provide you with the peace of mind you need to operate your vehicle, while knowing that you are being fully protected.

Having Access to More Options

Another way that working with an insurance agent can be beneficial is to help you to be aware of all of your insurance options – including having them help you find the best insurance rates. Additionally, since insurance brokers do not work for the insurer, they will work on your behalf to help ensure you have the most suitable and affordable vehicle insurance coverage.

Choosing the Right Insurance Agent

Now that you know more about the advantages of having an insurance agent at your side during this process, the next step is find out how to identify the best insurance broker for your needs. Here are some key pieces of information to help guide you during this decision-making process.

Do they represent a variety of insurance areas?

With car insurance being your current requirement, it is, of course important to look for an insurance agent that offers a variety of car insurance options. This is because you will want to ensure you have multiple options to choose from to help ensure you have access to a variety of rates as well as types of coverage.

Do they work with a variety of insurance companies?

Similarly, to the previous question, you will also want to find out if the brokers you are thinking of working with, have connections with multiple insurance companies. Again, this allows you to seek out a larger variety of insurance packages and rates, instead of being forced to go with higher rates and unsatisfactory coverage as your only option.

Do they work as a part of a team?

While in some cases it can be nice to build a relationship with one agent, it may also serve you better in the long run if they work as a part of a team. That way, if your agent is unavailable, they can leave you in good hands as you continue to access the insurance services as required.

While there are definitely some other questions you will want to ask, this is a good place to start. By taking the time to do your ‘homework’, you have the opportunity to gain a greater understanding of how insurance agents can help, as well as a more clear path forward in identifying which insurance agent will be the best fit.

Prior to making your final decision, you can also look into the reputations of the insurance agents. With this information on your side, you can feel more confident in choosing who you feel is the right insurance agent for your individual needs.

When all is said and done, it is important to trust the insurance agents you are working with. Contact Leaders Insurance to find out more about the role we can play in helping you to navigate your search for most comprehensive and affordable vehicle insurance package.

How to Protect your Deck & your Investment

How to Protect your Deck & your Investment

With nicer weather on the way, BC residents can look forward to spending even more time outdoors, including enjoying relaxing on their backyard decks. With this pastime to look forward to, keep in mind that you will want to take the time to protect your deck from various elements that can cause unwanted impacts, such as deck rot.Here are some steps you can take to help keep your deck in top condition as we move into the warmer seasons and can help you protect yourself - and your home, in the long run.

Perform Regular Deck Maintenance

First of all, it is also important to keep up-to-date with outdoor maintenance around your home and your deck should also be a part of this routine. Not only is this an investment in your home, it is also a situation, if not maintained can lead to you becoming liable. in the event someone is injured while spending time on your deck. A slip or fall incident and yes, even a deck collapse could lead to an unwanted accident and legal issue.

To avoid this, you can start by examining your deck for any evidence that might point to deck rot. With this, you should be on the look out for signs of damaged or rotted wood. These can include such any change in its appearance, such as discolourations to the wood, for example any darker or lighter patches.

With a watchful eye, you can also scan for gaps in the deck, where the wood will have likely shrunken. These signs can appear for reasons that include the wood becoming softer, spongier to the touch, as well as where it might also be crumbling or cracking. The paint may also display signs of wear and tear that can signify deck rot, and can present as bubbled or flakey surfaces.

One other way to identify whether you are dealing with deck rot is to use another one of your senses – that being smell. If deck rot is occurring, it is also highly likely that it will give off a musty smell, as the wood will have become damp due to excess moisture.

At this stage of the process, hopefully you have identified the problem earlier enough so that the deck rot can be treated. However, making sure your deck is a safe space for yourself and visitors should be a top priority.

Have Your Deck Inspected

Another method of ensuring your deck is well-maintained is to have it inspected by a professional. Not only can they let you know if it’s in solid condition, they can also help to point out if it is not and where repairs – or even replacement might be necessary.

A large part of this process also includes the inspection of the quality of the construction and the materials. This can particularly include an examination of the type of lumber that was used to build the deck, as these aspects should all be up to code.

If deemed that the proper materials and construction process was satisfactory, it is likely that a total reconstruction of the deck will not be necessary, however some prepares may be needed.

If deck rot is the cause of the damage, before the wood becomes too far gone, there are some steps to take to improve its condition. A part of this process will include, drying the deck and/or removing the source of the moisture. After this step, the wood can be re-treated with the proper products that will help to preserve the condition of the wood over time.

Ultimately, it is highly recommended that you also seek out more information from experts in this field to ensure you are taking the best steps to protect your deck.

Have the Proper Insurance

Not only do you want to protect the deck and outer perimeter of your home for a variety of important reasons, it is worth mentioning here as well that this moisture can also seep into the inside of your home.

For added protection of your home – inside and out – having home insurance to cover these types of damages as well as protect you from the possibility of being involved in an injury liability case, should warrant additional consideration for this type of home improvement investment.

At Leaders Insurance, we are here to help you protect all aspects of your home. Contact us to learn more about how home insurance policies can ensure you can make the most of your time as you look to spend more carefree time outside enjoying your home.

Avoid Getting Rear Ended & Take Precautions - Tips on how to avoid a domino collision

Avoid Getting Rear Ended & Take Precautions - Tips on how to avoid a domino collision

With the current BC weather fluctuating between warmer and colder weather, roadways have definitely kept drivers on their toes lately.While accidents can occur even on the clearest of days, recent icy weather conditions have caused some additional concerns when it comes to an increase in vehicle collisions in this region. In addition to smaller vehicles incidents, bad weather, among other unfavourable driving conditions can also lead to accidents that cause a chain reaction, involving multiple vehicles.

With that said, it is extremely important to be diligent and to follow the rules of the road, in order to protect yourself, your loves ones, as well as other drivers and their families. Read on to learn more about how to significantly reduce your risk of being involved in a rear end and/or domino collision.

Safe Driving Tips: How to Avoid Domino Collisions

Adhere to the Speed Limit

One of the best ways to avoid getting in a collision is to follow the speed limit. In this case, speeding can definitely lead to unwanted crashes when out of the roads, especially during poor weather conditions. When in combination with high volumes of traffic, inclement weather, and driving faster than you should, there is a higher risk of vehicle accidents that can lead to chain reactions.

As drivers, we should always adhere to the speed limits, as they are set for a reason. In the event you have to stop unexpectedly, if you are travelling at a slower speed, it is more likely that you will be able to stop in time and avoid a serious collision.

2. Maintain Distance Between Vehicles

In addition to speeding, not maintaining distance between other vehicles is another driving error that can commonly result in a major traffic accident. In fact, the ICBC actually states that when driving, it is necessary to keep to a distance that allows for two – three seconds of space between each driver and the vehicle in front.

They also go on to recommend that when operating a vehicle when road conditions are less than ideal, such as when visibility is partially hindered by fog or rain, drivers should remain at a distance of 4 seconds. In cases of more extreme weather, such as icy and snowy conditions, it is deal that this space be increases even further – and up to 6 seconds should be the norm.

In order to improve road safety and to reduce the occurrence of domino collisions, it is important that drivers keep their distance from one another, gauging the time between each other along with the nature of the road conditions at any given time.

3. Remain Alert/Avoid Distractions

This third safety tip reminds drivers of the importance of remaining alert at all times. It can only take a second and If you don’t watch the car in front of you, you could be the one to rear-end another vehicle.

This level of awareness is also important so that you are aware of how other drivers are operating their vehicles. Not only do you not want to cause an accident, you do not want to fall victim to a car crash as a result of the unsafe driving of others around you.

By maintaining alertness and distracted-free driving, this can significantly lower your chances of being in any type of car accident – especially one that leads to the domino effect and can place others safety in jeopardy.

4. Steer Clear of Larger Trucks

Lastly, in order to avoid dangerous outcomes directly related to unsafe driving, drivers can also be proactive and staying away from larger vehicles. Since it is just poor weather conditions that can restrict visibility when driving, so can driving behind or beside large trucks.

There are other reasons that trucks can be the instigators when it comes to collisions, such as the loss of cargo that can rather abruptly fall down onto the the road and even onto near by vehicles.

Either way, these types of dangerous incidents have been known to lead to major accidents, including the frequent occurrence of chain reaction crashes.

In the end, by monitoring your speed, maintaining distance between other vehicles, remaining alert, and avoiding driving behind big trucks, you can greatly reduce your risk of being in a car accident. These actions can also provide a greater sense of protection when it comes to avoiding the hazardous consequences that can result from being involved in a dangerous collision.

Ultimately as drivers, it should be our top priority to keep ourselves and each other safe while on the roads at all times. One other way to remain protected is to have the proper vehicle insurance coverage.

Reach out to our experts at Leaders Insurance to ensure you have the best insurance package for your needs and in turn, keep all aspects related to safe driving at the forefront of your mind each and every time you get behind the wheel.

ICBC Rebate - What Does This Mean for Me?

ICBC Rebate - What Does This Mean for Me?

Following up again on the upcoming relief plan for high car insurance rates in BC, ICBC is poised to make changes in order to improve the extremely high insurance premiums. These high rates, for some time now, have placed BC residents right smack at the top of the list of highest rates compared to all other provinces.As previously revealed, the 15% reduction in rates is set to take effect on May 1st, and in the meantime, there will be some financial relief coming very soon in the form of the ICBC rebate.

If you are a BC resident and car owner, read on to learn more about what these rebates will mean for you in the upcoming weeks.

Who is Eligible?

As a BC driver, if you had an ICBC insurance policy between April 1 and September 30, 2021, you are very likely eligible to receive this rebate. There are however some exceptions, such as individuals with lower insurance usage, for example in the case of those with vehicle operating permits that spanned less than 15 days. Rebate cheques are expected to be mailed directly to those who qualify beginning on March 15th.

The origins of the rebates stem from the reduction in collision claims made during this time period. As a result of the COVID-19 pandemic, and perhaps also due to less vehicle operations overall, the Crown corporation was able to save approximately $600 million this year. These excess funds are being re-directed back into the pockets of many BC car insurance policy holders in mere upcoming weeks.

How Much Will You Receive?

It is important to also mention that the exact rebate amount that you will receive will depend on the type of coverage you had. With that said, these amounts will average approximately $190 for each eligible BC driver falling into this category. Ultimately, this amount is a breakdown of the 19% that each policy holder paid between April and September of the last year.

Furthermore, the BC government has stated that these amounts will be automatically calculated based on the nature of each individual policy. It is significant to also note that these payments also reflect the largest insurance rebates that have historically been paid out across the entire country.

As BC drivers wait for the Utilities Commission’s 15% insurance rate decrease to take effect in May, this timely monetary support is on the way. The rebates, combined with these future lower premiums, will aim to make driving in this province more financially manageable.

For more details on this rebate, it is suggested that you reach out to your insurance broker for the most up-to-date information.

At Leaders Insurance, we are here to support you with your individual insurance needs. As a driver in BC, we can offer you the insurance policy that best reflects the right amount of coverage for your vehicle and for your peace of mind.

As the province looks forward to more affordable vehicle insurance premiums, you can reach out to us with any questions you have about your current policy, as well as your future insurance needs.

How Much Cheaper will BC Auto Insurance Rates be Now?

How Much Cheaper will BC Auto Insurance Rates be Now?

Owning and operating a car often proves to be a large financial responsibility for many Canadians. This is the reality and can be, in part, due to the costs associated with insurance fees.While these fees range from one province to another, one thing is for sure, car owners in BC, have been experiencing much higher than the national average when it comes to vehicle insurance rates.

Fortunately, some financial relief appears to be on the way. If you are a car owner in BC and are hoping to have access to more affordable insurance rates, read on to learn more about some of the latest developments in this area.

In a recent move by then BC utilities regulator, and as per a request by the Insurance Corporation of BC (ICBC), BC residents are soon to see a 15% reduction in all basic insurance rates.

The plan being, that this initial 15% decrease will act as a short-term percentage reduction and will begin on May 1, 2021. Following that, the province’s Utilities Commission will determine a more permanent rate moving forward.

With this being the most significant rate reduction in approximately 40 years, this definitely shows that there is some light at the end of the tunnel for BC car owners.

Insurance Rates Across Provinces

To fully put these high rates into perspective, the Insurance Bureau of Canada (IBC) reports BC annual average insurance rates as high as $1832. Next in line is Ontario, who sits at a slightly lower rate of $1528. In rather drastic comparison, we have Quebec with the lowest of these premiums at $717 per year.

With BC insurance premiums currently sitting at the highest among all other provinces, these reduced rates will look to ensure that BC residents also have access to more affordable vehicle insurance. Ultimately, this change is set to place them more on par with other provinces, like Ontario or even Alberta, who’s residents by comparison experience yearly rates of approximately $1316.

How Will Drivers Save?

This move not only looks to lower these rates, however, it also involves the reallocation of substantial funds, in the hundreds of million dollar range. Currently, these finds are being used towards insurance legal fees, and moving forward, they will be used towards cases where individuals have sustained injuries as a result of vehicle collisions or crashes.

Overall, it is expected that these changes will translate into a 20% reduction in provincial premium claims, with an average decrease of $400 each year.

Insurance Rebates

Another move made by the ICBC will see rebates being offered to drivers to offset the cost of current rates as a stopgap until May, when the lower rates take effect.

While these rebates will still have to go through one final approval process with the provincial insurance commission, there is reason to remain positive that BC drivers we be able to take advantage of the rebates as soon as possible as more affordable insurance rates are just around the corner.

Turning to an insurance expert is an effective way to learn even more about these upcoming changes.

At Leaders Insurance, we are here to provide the most up-to-date information on car insurance premiums in BC. Contact us to learn more about these developments and together, we can find the car insurance package that is right for you.

What is a Business Continuity Plan & Why is it Important for your Business?

What is a Business Continuity Plan & Why is it Important for your Business?

As a business owner, there are many factors to consider when keeping your operations running smoothly. That said, the past year has been unlike any other, we as a society, have experienced in recent times.Part of ensuring that your business continues to operate during times of upheaval, such as other types of sudden events like natural disasters, ice storms, fires, and floods, etc. - it is critical to have what is known as a Business Continuity Plan.

Business Continuity Plans are crucial to a company’s ability to survive and be sustainable during times of crisis that would otherwise significantly interrupt and impede their day-to-day operations. On the other hand, companies who have the foresight to put key plans in place, in order to offset the devastating consequences that these types of occurrences, can go on to operate another day.

Fortunately, as a business owner in Canada, you are not alone in making these vital and strategic decisions. Public Safety Canada, through the Government of Canada has helped by outlining some key aspects of this process.

First of all, it is suggested that you start by identifying the severity of these types of potential threats to your business. Next you can look at narrowing down which specific ones will require that you implement a proactive plan. It is also important to determine which of these aspects will require documented follow-up tasks, and what steps will need to be taken as a result.

Here are some valuable considerations you can ask yourself as you begin to develop your own business continuity plan model.

Do you have enough Insurance?

Another fundamental part of this plan is to ensure you have the right insurance coverage for your business needs. In your business continuity plan, you will want to examine your current insurance coverage and make sure that it will include these types of events and will adequately cover the cost of any major potential losses you could encounter.

It can also be equally important to look at whether you are overinsured in any areas that perhaps will not pertain to your business. Ultimately, at this stage as well as on a regular basis, it is important to reevaluate your business insurance coverage in order to ensure your continuity plan is highly reflective of your business operations, not to mention a proactive plan for future sustainability.

In the event of a disaster and when the continuity plan needs to be implemented, it is necessary to set up a method for informing your business associates, staff, suppliers, and clients. Safety procedures are also a part of these plans, so that the well-being of staff and clients are maintained, and business operations and connections are preserved as much as possible when and if, the time comes that the continuity plan must be activated.

As you act to either develop or re-visit your Business Continuity Plan, it is important to understand that having the right insurance can also play a large role in the success of this plan.

One step you can take right now is to reach out to your insurance broker to discuss your current insurance coverage. Contact Leaders Insurance to find out more about how we can contribute to the successful future of your business.

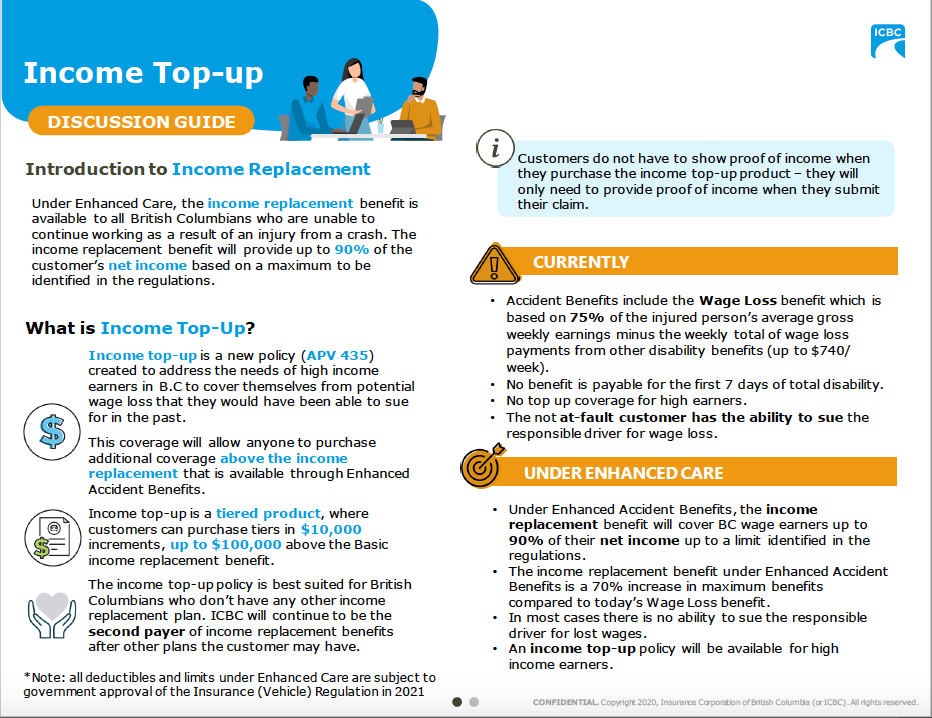

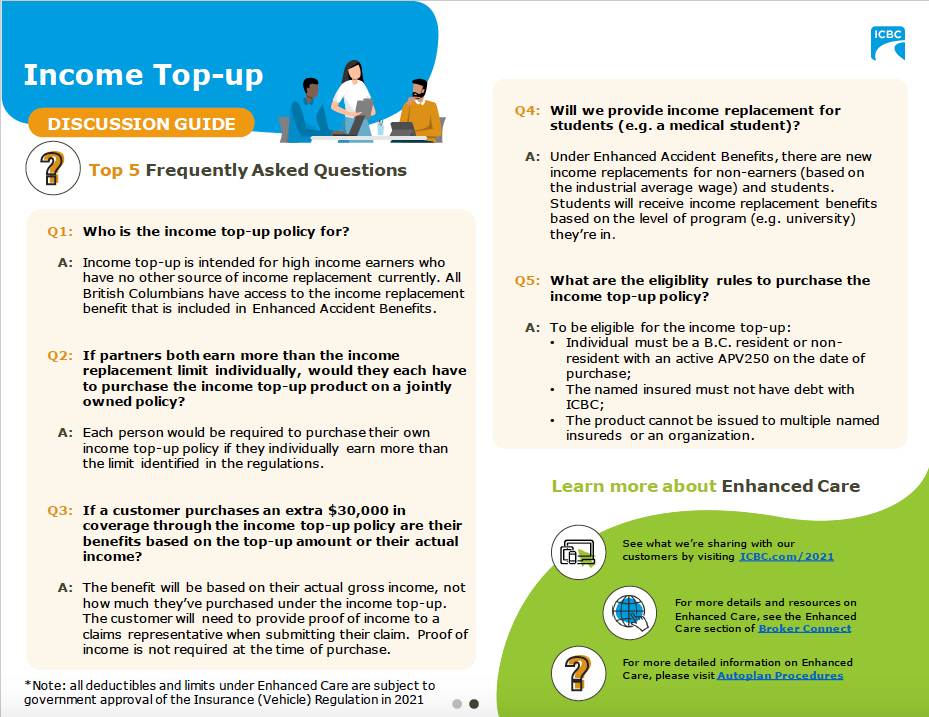

NEW Enhanced Care Coverage Offered by ICBC - starting May 2021

Starting May 2021, ICBC will be offering Enhanced Care Coverage which is a Income Top-Up program for individuals involved in an accident where they will have loss of work. To find out more, please contact us at 604-469-1799 or read the information sheets below -

For more information on Enhanced Care, click here.

How to Insure a Vacation Home in 2021

How to Insure a Vacation Home in 2021

Do you own a vacation home? If so, then 2021 as well as its predecessor, may have posed some additional challenges for you with regards to either operating it as a rental or being able to spend some time there, yourself. Hopefully this will improve as we move further in 2021, however, one factor still remains the same, you will need to continue to have this property adequately insured.Here are a variety of scenarios that may relate to you and your vacation home and the steps you can take to ensure you have the proper home insurance policy to meet your ongoing needs.

For starters, to help determine the type of insurance you need, one key consideration is how often you will be living there. For example, if this is your secondary residence, then it is important to know that it is likely that you will be paying a bit more for insurance costs. In some cases however, you may be able to include your vacation home insurance in the same policy with your primary residence coverage.

To better identify how best to insure your vacation home, you can review the following vacation home occupancy scenarios and see which one(s) best reflect your insurance needs.

Insuring a Home You Are Not Renting Out

If you own a vacation home that you are not going to be renting out, then your primary home insurance coverage may not include this type of coverage. This is because primary residence insurance policies typically only relates to homes that are being regularly occupied.

For example, if this home will be unoccupied for more that 30-90 days at a time, you are likely to need to take on some additional coverage to include in your home insurance package. Speaking to your insurance broker is the best course of action, so that you make sure you have enough secondary coverage.

Insuring a Home You Will Occasionally Rent Out

This second scenario includes the times when you plan to rent out your secondary residence on an occasional basis. Perhaps you will rent out your vacation home as an occasional Airbnb, or to friends and family a couple of times a year.

If this is the case, then your original and standard home insurance policy might cover this type of arrangement as well. With that said, again you will want to discuss this with your home insurance broker to ensure you have the right coverage for your needs.

Insuring a Home You Will Regularly Rent Out

This last rental arrangement, as the heading states, is for secondary vacation homes that will be rented out on a regular basis. Unlike the other two scenarios, if this is your plan, it is highly likely that you will need to add some additional coverage onto your original policy.

Here are some of the types of supplemental coverage you may need, depending on your circumstances.

Short-Term Rental Insurance Coverage:

Otherwise known as home-share coverage, this vacation home insurance policy option is typically a type of insurance for those who are renting out their homes as an Airbnb or for shorter periods of time. In this type of arrangement, adding coverage to your original policy is the likely to be necessary. It is advisable that you check with your broker make sure you have enough insurance for the correct length of time for these shorter rental periods.

Long-Term Rental (Landlord Insurance) Coverage:

This type of coverage is used more in the cases of longer-term rentals, however sometimes can also apply to short-term tenants as well. If there is the potential that you will be renting out your vacation home for longer stretches of time, then choosing this comprehensive insurance package might be the more affordable option. This insurance policy reflects a separate insurance package on its own to ensure that as a homeowner you are adequately covered for these types of rental agreements.

In the end, the best way to protect your vacation home is to first, identify how you plan to rent out your vacation home in the future. Additionally, since these types of insurance policies can vary across different insurance companies, you will want to examine these policies closely with the help of your insurance broker.

At Leaders Insurance we want to ensure that our clients have the most up-to-date information regarding their insurance policies. If you are looking to insure your vacation home this year, contact us so that we can align your home insurance coverage with your specific needs.

What is a Communicable Disease Exclusion on your Home Insurance?

What is a Communicable Disease Exclusion on your Home Insurance?

If you are a homeowner, it is likely that you have already given a lot of thought to the type of insurance you need. With that being said, these days, we have had to expand our scope more than ever to also factor in issues related to COVID-19 and pandemic home insurance claims.There is a component of home insurance that covers Communicable Disease Exclusion, and while in the past, this has been rarer, during these unprecedented times, some insurance companies have opted to include this in their home insurance policies moving forward.

Currently this type of insurance feature has been closely related to the COVID-19 claims that insurance companies are more likely to encounter. For example, in the event a person files a claim that they have been infected with COVID-19 or another communicable disease in the home of another individual, they could feel they have grounds to sue the individual whom feel is responsible, particularly if they have become severely ill as a result.

While in many parts of Canada, there have been strict rules in place for limiting gatherings, particularly within homes. This type of cross-household contact has been identified as one of the common methods of COVID-19 transmission.

On the other hand, many Canadians have taken the necessary precautions and done everything possible to avoid the spread of COVID-19. With that said, individuals could still have gone on to contract the virus and in some cases, they may look at tracing it back to a certain social gathering or interaction they had within a particular household.

While it can be a challenge to prove these types of cases, the bottom line is, that this could be an expensive outcome for homeowners. Therefore, turning to this type of home insurance coverage may definitely be worth examining further.

Ultimately, with this Communicable Disease Exclusion in place, your home insurance policy can cover these types legal expenses. It is recommended that you do reach out to your broker to find out if this is already included in your policy, and if not, perhaps adding this your home insurance package could be of great benefit to you.

In the end, what this really comes down to is the importance of having a full understanding of your home insurance policy. By having a better grasp of all of the features and specific types of coverage, as a homeowner, you can have the added peace of mind you need to effectively navigate the responsibilities of homeownership, especially during these extremely challenging times.

At Leaders Insurance, we are committed to making sure our clients are informed and fully satisfied with their insurance coverage. Contact us today to learn more about the Communicable Disease Exclusion for homeowners, and let us help to ensure you are set up with the best home insurance policy that covers all of your needs now and into the future.